After working with and studying many busy entrepreneurs, I found that most small business owners are great at what they do, but don’t understand the numbers. Or, they don’t know what they don’t know, and are overwhelmed trying to learn the business and financial side of running a business. I took these common mistakes, knowledge gaps, and case studies and shared a step-by-step solution through my bestselling book, Small Business Finance for the Busy Entrepreneur – Blueprint for a Solid, Profitable Business.

Since the book launch, I’ve been asked to give my signature talk, “7 Secrets to Financial Success for Small Business Owners.” The audience’s feedback on the most surprising tip or lesson learned has been consistent, from both aspiring entrepreneurs and experienced business owners. Based on that feedback, I created this Ultimate Guide to share the exact steps to organizing your business finances to make your life easier.

What you’ll get:

- Get step-by-step instructions with tips to keeping more money in your pocket (and business) with this comprehensive 12,000+ word guide.

- Understand what the IRS and your CPA want, so tax day is a piece of cake and you avoid IRS fines.

- Know exactly what to do and when, so you can stay sane while running your business.

Ultimate Guide to Organizing Your Business Finances

Why I Wrote This Guide (And Why It’s Important)

I’ve been in your situation where the IRS rules seemed too confusing and I didn’t really understand what my CPA needed or wanted. I looked up answers on my own by searching the Internet, reading books, attending seminars, asking financial colleagues, and interviewing multiple CPAs. In the end, I’ve gathered and paid for knowledge that took over two years to accumulate and process, and I’m sharing the best tips in this guide.

That’s why I wrote this guide. This guide will cover in ONE place how and why it’s so important to organize your business finances in a way that will keep more money in your pocket, help you avoid IRS fines, and allow you to stay sane while running your business. I want to save you the time and money to get better organized, set-up a system that works the first time, and allow you to focus on what’s most important – running your business!

What this Guide Will Cover and What It Won’t

First, I will cover the basic three steps you need to absolutely do first when you start a business, to create the foundation to being organized. Next, I’ll tell you why the #1 secret to being organized is to separate your business and personal finances. There are legal, financial, and emotional consequences if you commingle your business and personal money, and I’ll share why there are NO exceptions to this.

I’ll cover the bank accounts you should absolutely have, why business credit card are great for your business, how to overcome the fear of being audited (and what the IRS really care about), what you should really care about when it comes to taxes, how to do your taxes the right way (and not accidentally cheat), can you really write-off your home office, best system to keep track of your business expenses and receipts, how to make tax day a piece of cake, and how to survive being audited by the IRS.

In this guide, I won’t be covering the different account software tools that are available. There are several good ones out there, but many small business owners will pay for a monthly subscription to one that their CPA or friend recommended, but don’t know how to use it. Then, they don’t even open the tool or use it correctly because they get overwhelmed with the numbers and tool. Therefore, what this guide will do is provide you the foundation for knowing what numbers you need to track and keep organized, regardless of what tool you use. Once you’ve created this foundation, you’ll be ready to move on looking at different tools to automate the process.

How to Read this Guide (and Which Chapters to Read If You’re in Crunch Mode)

If the idea of reading a 12,000+ word Ultimate Guide seems too daunting and you’re pressured to quickly gather all your information to meet with your CPA, then focus and read the following Chapters and sections first:

Chapter 2: Separate Your Business and Personal Finances (or Pay the Price)

- Chapter 2.4: What to do now if you’ve already mixed business with personal

Chapter 5: How to Do Taxes the Right Way (and Not Accidentally Cheat Yourself)

- Chapter 5.1: Deducting All Eligible Business Expenses (to Keep More Money in Your Pocket)

- Chapter 5.2: Confirming What’s Ordinary and Necessary to Your Business

- Chapter 5.3: Home Office: Can You Really Write It Off?

Chapter 6: Best System to Keep Track of Business Expenses & Receipts

- Chapter 6.2: Who to Outsource to If You Hate Dealing With the Boring, Admin Stuff

- Chapter 6.3: How to Not Tear Your Hair Out When Providing Proof for IRS Audit

- Chapter 6.4: How to Fool-proof Your Receipts

Chapter 7: How to Pay Your Taxes, and Not a Penny More

- Chapter 7.1: Don’t Overpay Your CPA

Chapter 8: How to Make Tax Day a Piece of Cake (and Eliminate Need for Tax Extensions)

- Chapter 8.1: Top 10 List When Meeting Your CPA

Chapter 9: Overcome the Fear of Being Audited (and Learn What the IRS Really Cares About)

- Chapter 9.1: Income You Made

- Chapter 9.2: Income You Paid to Independent Contractors

- Chapter 9.3: Taxes Are Paid

- Chapter 9.4: How to Prove You Didn’t Cheat, Lie, and Steal

Once you’ve gotten out of crunch mode, then go back through and read the Ultimate Guide in order, especially all of Chapter 2: Separate Your Business and Personal Finances (Or Pay the Price) and Chapter 3: The 3 Types of Bank Accounts You Should Absolutely Have. Often, I’ve found the root cause of a lot of headaches, fines, and overpayment to the IRS and CPA are a result of not separating your business and personal finances, and not have these three types of bank accounts.

If you’re just starting out in your business or if you’re reading this guide for tips on how to become better organized for next tax season: You’re in the perfect position! Read the chapters in order and learn the exact steps to take to keep more money in your pocket, avoid IRS fines, and stay sane while running your business!

There is a lot of content in this 12,000+ word Ultimate Guide. To make it easier for you to read and implement, I’ve created the PDF version of this guide for you – you can download it, save it to your computer or iPad, or print it to make notes. With the PDF version, I’ve also included a BONUS step-by-step checklist that will help you overcome challenges like, “I don’t know where all the money is going,” “I don’t have enough time,” and “I had to pay a late fee with interest.” This bonus Financial Admin Day (FAD) checklist is included at the end of the Ultimate Guide.

Table of Contents

Below you’ll find a table of contents with everything that’s included in this 12,000+ word guide. You can either go through it step by step (I highly recommend this) or skip to the part that’s the most interesting to you if you have limited time.

Here’s what you’ll learn from this guide:

Chapter 1: 3 Steps You Absolutely Need to Do First When You Start a Business

Chapter 1.1: Choose the Right Legal Entity

Chapter 1.2: Obtain a Tax Identification Number

Chapter 1.3: Apply for a Sales Tax Identification Number

Chapter 2: Separate Your Business and Personal Finances (or Pay the Price)

Chapter 2.1: Legal Consequences When Mixing Business with Pleasure

Chapter 2.2: Financial Hit When Blurring the Lines of Personal and Business

Chapter 2.3: Emotional Result When Business and Personal Finances Are a Mess

Chapter 2.4: What if I’ve Already Mixed Business with Pleasure?!?

Chapter 3: The 3 Types of Bank Accounts You Should Absolutely Have

Chapter 3.1: What You’ve Never Thought to Do with Your Business Accounts

Chapter 3.2: Purpose of Each Bank Account

Chapter 3.3: The Best Banks for Small Business Owners

Chapter 4: Why Business Credit Cards Are Great

Chapter 4.1: The Difference between Business and Personal Credit Cards

Chapter 4.2: Top Reasons Why a Business Credit Card is Better Than a Debit Card

Chapter 4.3: What are the Best Business Credit Cards?

Chapter 5: How to Do Taxes the Right Way (and Not Accidentally Cheat Yourself)

Chapter 5.1: Deducting All Eligible Business Expenses (to Keep More Money In Your Pocket)

Chapter 5.2: Confirming What’s Ordinary and Necessary to Your Business

Chapter 5.3: Home Office: Can You Really Write It Off?

Chapter 6: Best System to Keep Track of Business Expenses and Receipts

Chapter 6.1: Top 3 Reasons Why You Need to Use the Cloud

Chapter 6.2: Who to Outsource to If You Hate Dealing with the Boring, Admin Stuff

Chapter 6.3: How to Not Tear Your Hair Out When Providing Proof for IRS Audit

Chapter 6.4: How to Fool-Proof Your Receipts

Chapter 7: How to Pay Your Taxes, and Not a Penny More

Chapter 7.1: Don’t Overpay Your CPA

Chapter 7.2: Who You Should Hire and Have in Your Corner

Chapter 7.3: Frequently Asked Questions

Chapter 8: How to Make Tax Day a Piece of Cake (and Eliminate Need for Tax Extensions)

Chapter 8.1: Top 10 List When Meeting Your CPA

Chapter 8.2: How to Get the VIP Treatment from Your CPA

Chapter 8.3: Create a Financial Admin Day (FAD)

Chapter 8.4: How to Never Miss an Important Deadline

Chapter 9: Overcome the Fear of Being Audited (and Learn What the IRS Really Cares About)

Chapter 9.1: Income You Made

Chapter 9.2: Income You Paid to Independent Contractors

Chapter 9.3: Taxes Are Paid

Chapter 9.4: How to Prove You Didn’t Cheat, Lie, and Steal

Chapter 10: How to Survive Being Audited by the IRS

Chapter 10.1: 3 Types of Audits

Chapter 10.2: Bring It On – What You’ll Need in an Audit

Chapter 10.3: Possible Outcomes from an Audit

Chapter 10.4: Why Hiring a CPA to do Your Taxes is the Best Choice

Chapter 1: 3 Steps You Absolutely Need to Do First When You Start a Business

Make sure you are setting yourself and the business for success from the beginning by doing these three steps when you start a business:

- Choose the right legal entity for your business

- Obtain a tax identification number (TIN) – also known as employer identification number (EIN)

- Apply for a sales tax identification number from the state(s) you plan to sell products in

Chapter 1.1: Choose the Right Legal Entity

It makes me cringe when I hear people are running their business as a sole proprietorship. It also makes me frustrated when I hear that many small business owners were told by their CPA that they can just run their business as a sole proprietorship until they are making a certain amount in profit.

This is NOT true.

A sole proprietorship is NOT a legal entity. Consult with a business lawyer to confirm what legal entity is right for you. At a minimum, you should register your business as a limited liability company (LLC) to keep the business as a separate entity from yourself. This provides one of the cheapest forms of insurance for your business. When you create your LLC, this allows the business to be separate from you – your personal name, your personal assets, and your family. Otherwise, in a sole proprietorship, you and the business are ONE, using and providing your social security (SSN) for business. If someone decides to sue your business, then your personal assets can be at risk, including your home, car, and personal bank accounts. Give yourself (and your family) the piece of mind by setting up your business as an LLC.

Don’t let anyone tell you that it will cost more for your CPA to do your taxes as an LLC versus a sole proprietorship as a deterrent from applying for a legal entity. It should cost the same since the same IRS form is used for both when reporting income and expenses – Schedule C (Form 1040) – because in the eyes of the IRS, a sole proprietorship and LLC are treated the same for tax purposes. However, from a legal standpoint, they are very different.

Chapter 1.2: Obtain a Tax Identification Number

After you’ve decided on your legal entity and registered your business name with your state, then apply for an Employer Identification Number (EIN) from IRS.gov. It doesn’t cost any money, so don’t be scammed by sites that charge for an EIN. You will need this EIN when you open business bank accounts, which need to be separate from your personal bank accounts.

(*Note: More about separating your personal and business finances and opening business bank accounts will be covered in Chapter 2: Separate Your Business and Personal Finances (or Pay the Price) and Chapter 3: The 3 Types of Bank Accounts You Should Absolutely Have.)

Chapter 1.3: Apply for a Sales Tax Identification Number

If you plan to sell any products and goods, you need to apply for a sales tax identification number with the state(s) that you conduct business in. This is a completely different number than the tax identification number (TIN) that you obtained from the federal government. Go to the secretary of state’s website for details on how to apply and when sales tax collected are due for your state(s).

Chapter 2: Separate Your Business and Personal Finances (or Pay the Price)

One of the most important things you can do as a small business owner is to separate your business from your personal finances. This means having separate bank accounts and credit cards for the business and its expenses. You should avoid using your personal credit card to pay for both business and personal expenses. Similarly, never using your business credit to pay for personal items. Otherwise, there are legal, financial, and emotional consequences when you commingle the two.

Chapter 2.1: Legal Consequences When Mixing Business with Pleasure

If you are routinely commingling your personal and business accounts, or using business assets for your personal benefit, you can lose the legal protection that was set-up for your business. This is also commonly referred to as piercing the corporate veil. In this case, if someone decides to sue your business, you can be held personally liable for the business debts and your home, bank accounts, personal investments, and other assets can be used to pay off the corporate debt. Therefore, never mix business with pleasure and keep all your expenses separate.

Chapter 2.2: Financial Hit When Blurring the Lines of Personal and Business

If you are using both your personal credit card to pay for business expenses, it is easy to overlook recording business expenses that were on your personal credit card. The unfortunate result is that you lose out on claiming that business deduction. In other words, you paid more taxes than you really owed. Separate accounts help you to be sure you are deducting all eligible business expenses, which will save you both time and money.

If you use your business credit card to pay for personal expenses, then it can lead to incorrectly claiming a business expense that was truly a personal item. There are financial consequences if you are audited by the IRS, because this means you paid fewer taxes than you owed. While it may be an honest mistake, the government will slap a penalty and calculate interest starting from the date you should have paid taxes on those expenses. This could mean interest that is calculated back from three to five years! Avoid taking a financial hit by never blurring the lines of personal and business.

If you’ve decided to hire a bookkeeper or CPA to sort through all the transactions to find all the legitimate business expenses between the accounts, this can lead to a very expensive bill since they will likely bill you by the hour! One of my CPA colleagues told me that he once had to sort through 10,000 bank transactions to separate business from personal. At a bill rate of $200 per hour, the business owner had to pay an additional $800 in tax preparation fees!?!

Chapter 2.3: Emotional Result When Business and Personal Finances Are a Mess

When you commingle your personal and business finances, there is no clear picture of how your business is doing financially. When the finances are a mess, this can cause unnecessary stress and strain on the relationship with your family and significant other. If you accidentally take money that was meant to cover personal expenses such as the mortgage, childcare, groceries, etc. and use it for the business, that can cause resentment when the financial burden impacts your significant other and family. It’s very difficult to see the financial health of the business versus family when all the money is all being put into and managed from one bank account.

You can also waste hours trying to sort through bank and credit card transactions, and open yourself up to an IRS nightmare. Eliminate the potential for stress by keeping clean financial records for your personal and business finances.

Chapter 2.4: What if I’ve Already Mixed Business with Pleasure?!?

If you’ve already been mixing your business and personal finances, don’t panic. You can still correct everything and get on the right path. If you’re reading this and it’s crunch time with tax preparation, then just do first step below. When you have time, go back and do the second step.

The first and most important step is to look through your business bank account and credit card transactions, and go line-by-line through all the transactions. Make sure you can validate with a receipt that each expense is a legitimate business expense. If you’ve been using your business bank account and business credit card to purchase personal items as a form of “pay day” to yourself, then flag those expenses and be sure to tell your CPA that these were personal items. Depending on your business legal entity, it may get treated as an owner’s draw or member distribution. The most important thing is that these expenses are not reported as a business deductions, which would incorrectly lower your business income, and result in you mistakenly paying less taxes than you owed.

The second step is to go through all your personal bank account and credit card transactions, and look for any business expenses that were charged. Spending time to sort through and find these transactions can allow you to ensure you’ve deducted all eligible business expenses, legitimately lowering your business taxable income and tax liability. In other words, you avoid paying more taxes than you really owe.

Chapter 3: The 3 Types of Bank Accounts You Should Absolutely Have

Do you have separate personal bank accounts that have different purposes and use? Most people have at least one personal checking and one savings bank account, so they can mentally and physically see the money allocated for living expenses versus savings goals (i.e. emergency fund, vacation fund, college fund, etc.) This helps eliminate running out of money or guilt in spending on things that may not be immediate, monthly expenses like emergencies, vacations, and college education.

Chapter 3.1: What You’ve Never Thought to Do with Your Business Accounts

Most people see the value and already separate their personal finances into multiple accounts, but that same thinking doesn’t always get transferred over to business accounts. By having all the money for the business sitting in one checking account, this can result in business owners running out of money to pay for taxes and not having any reserves for emergencies, because it’s easy to think that there is more money to spend and invest in the business when all the money is all in one checking account.

That’s why I recommend that all business owners open three bank accounts – two checking accounts and one savings account. This way there is enough money when it comes to paying the monthly operating expense, taxes, and any emergencies or future investments.

Chapter 3.2: Purpose of Each Bank Account

The first checking account is for the operating expenses. This is for all the monthly bills that you have to pay to keep the business running, including payroll, monthly dues and subscriptions, and utilities.

The second checking account is for taxes. For the revenue that comes into your operating expense checking account, transfer enough money into this account to cover your tax liability. Do this on a monthly or bi-monthly basis, and keep it a consistent date (i.e. 7th of every month) or day of the month (i.e. last business day of the month). If you don’t know how much you need to be saving each month, consult with a CPA to calculate your tax rate and estimated taxes. To be on the safe side, assume and start saving 25% for taxes until you meet with a CPA.

And the third bank account you need is a savings account for business emergencies and savings for future business investments (i.e. equipment, conferences, property).

Chapter 3.3: The Best Banks for Small Business Owners

The best bank for most small business owners is one that offers accounts with zero to low monthly maintenance fees, no required or maximum number of transactions needed per month, and no monthly balance requirements. Don’t assume that it’s easier or better to open a business bank account at the same bank as your personal bank accounts. You will want to look at the monthly maintenance fees, monthly number of transactions and cash deposits allowed, and average monthly or daily balance requirements to determine which bank is best for you and your business.

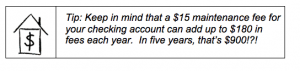

If you are just starting out in your business, you don’t want to be tied to maintaining an average monthly balance of say $5,000 or more or be forced to spend at least $250 in net new purchases to avoid a $15 per month maintenance fee (*Note – this is an example based on a Business Fundamentals Checking account at Bank of America.) Otherwise, if you are consistently not meeting the requirements, you could be paying $15 x 12 = $180 in fees each year! Or worse, you’d be forced to spend $250 each month, regardless if you need the items, just to avoid a $15 maintenance fee.

I have found that the regional and community banks tend to be friendlier to business owners, as opposed to the bigger, national banks. If you’re not sure which ones to look at, check to see if Capital Bank, First Citizens, and BB&T are in your area. Credit unions can also be a good choice, but not all offer business checking accounts. Don’t assume you can use a personal checking account for your business because it can affect your legal liability and some banks may automatically close your account if they find out you’ve been using it incorrectly.

Chapter 4: Why Business Credit Cards Are Great

Some people don’t believe in credit cards and feel like cash and debit cards are safer. However, while they may help you to avoid debt by not allowing you to charge more than you have, I believe that business cards are safer and offer great benefits for business owners, especially for those who can budget and pay off the balance each month.

Chapter 4.1: The Difference between Business and Personal Credit Cards

The biggest difference between a business and personal credit card is that interest rates can change frequently and without notice, because the Credit CARD Act of 2009 doesn’t apply. With personal credit cards, the interest rates and fees are capped due to this law. If you pay your balance in full every month, then this should be a non-issue.

With new business owners, since you don’t have a credit history, most likely the credit bureaus will look at your personal credit score, so you can be held personally liable for the debt. Unfortunately, your account history may not always be reported back to the three major credit bureaus, so good behavior and responsible payment history may not improve your credit score with a business card.

Regardless if your credit score improves with a business credit card, big perks of business cards are the rewards, which can include cash back, travel points, and tailored bonus rewards based on specific categories such as office supplies, advertising, and Internet purchases.

Most importantly, as discussed in Chapter 2: Separate Your Business and Personal Finances (or Pay the Price), you want to keep your personal and business purchases separate and the easiest way to do that is to open a business credit card for business expenses only.

Chapter 4.2: Top Reasons Why a Business Credit Card is Better Than a Debit Card

While it may sound like a great idea to only use a debit card to help you avoid spending more money than you have, there are three reasons why a business credit card is better (and safer) than a debit card, including:

#1 – Liability is limited when using a credit card.

- If you report fraud on your credit card, your liability is limited to up to $50 for the fraudulent charges. However, with a debit card, you typically only have up to two business days to report the charges to limit your liability to up to $50. Your liability increases to up $500 if you report after two business days but within 60 days of receiving a bank statement that includes the unauthorized charges. If 60 days have passed since you received a bank statement, then your liability is unlimited and you owe the full (*Note – Some states and banks may vary on their liability limits.)

- Places you should avoid using a debit card in particular because of reported skimmers being attached included gas stations and ATM machines. These skimmer devices allow thieves to steal your card number and PIN.

#2 – Not all places accept debit cards, including rental car companies.

- Rental Cars – some rental car companies do not allow you to book a reservation with a debit card. They will allow you to pay with a debit card, but will require a credit card to make the reservation. More importantly, even if you find a company that allows you to reserve with a debit card, they will typically put a hold on your debit account for an amount GREATER than your reservation in case you keep the car longer than expected or if there are damages. Depending on your account balance, this can cause overdraft fees if checks or charges bounce, especially since the holds don’t fall off until several days (often 48 hours) after the reservation.

- Real life story – Here’s a great personal story from my FinCon colleague, Jessica Garbarino, Owner of Every Single Dollar, on the many challenges of trying to rent a car at the airport with her debit card when her car broke down: Read the Fine Print

FinCon colleagues (L-R): Belinda Rosenblum, Jessica Garbarino, me, and Sarah Li Cain

#3 – Large holds don’t affect your account balance.

- Rental car companies and hotels will often place a hold on your account for an amount greater than your reservation to cover any damages and incidental charges. If you’re using a credit card, this typically won’t affect you and by the time you need to pay your statement balance, these extra hold charges have been taken off. However, if you’re using a debit card and don’t have sufficient funds to cover these holds (that may take up to a week to fall off), your bank will charge overdraft fees and you’ll get hit with fees for any bounced checks.

Do yourself a favor and for the peace of mind, use a business credit card to pay for your business expenses. Then, budget and make sure you have enough funds in your business checking account to pay your credit card balance in full if you want to avoid interest charges.

Chapter 4.3: What are the Best Business Credit Cards?

If you’re interested in which business credit cards to consider, my financial colleagues tend to like Chase Ink Business (5x phone and office supplies), Costco Anywhere Visa Business (4x gas, 3x dining & travel) and Capital One Spark Cash (2x on everything).

If you’re still confused based on the different annual fees and perks, check out this blog post by my colleague, Lee Huffman, with BaldThoughts: 5 Tips to pick the best business credit card.

Lee Huffman visits Raleigh FinCon group

Chapter 5: How to Do Taxes the Right Way (and Not Accidentally Cheat Yourself)

Regardless of who prepares your taxes or what software you use, you should become reasonably informed on how to do your taxes and not accidentally cheat the government out of its money. While a CPA will prepare your taxes, they will make you sign a disclaimer that you provided complete and accurate information and that you can’t hold them accountable for inaccurate or missing data. Most importantly, make sure you aren’t cheating yourself out of deducting expenses that the government has allowed you to legally claim.

The first step to know all the possible types of business expenses and then confirm with a CPA that these expenses are considered ordinary and necessary to operate your business.

Chapter 5.1: Deducting All Eligible Business Expenses (to Keep More Money In Your Pocket)

To keep more money in your pocket, you need to reduce your taxable income by deducting all your eligible business expenses. The easiest and quickest way to learn what expenditures qualify for business deductions is to look at the IRS Form – Schedule C (Form 1040) for Profit or Loss From Business and refer to Part II Expenses section.

Screenshot of Schedule C (Form 1040) for Profit or Loss From Business from IRS.gov

Also, for general rules for deducting business expenses and specific expenses, refer to the IRS Publication 535: Business Expenses.

Examples of business deductions listed in the IRS Schedule C (Form 1040) are: advertising, legal and professional services, office expenses, rent or lease, repairs and maintenance, supplies, meal and entertainment, and travel.

Chapter 5.2: Confirming What’s Ordinary and Necessary to Your Business

Regardless of your legal entity, the types of business expenses are the same. However, you will only be allowed to deduct business expenses that are ordinary and necessary to your business.

What does that mean?

- Ordinary Expense = common and accepted in your trade or business.

- Necessary Expense = one that is helpful and appropriate for your trade or business.

- For example, if you owned an IT company and offered consulting services, you could probably justify that it is ordinary and necessary for you to purchase multiple brands and versions of cell phones and laptops to ensure that any software programs that you create will work across all the different platforms (i.e. Apple versus Microsoft products) and models. However, if you owned a real estate business, that same reasoning will likely not work with the IRS.

There is a separate section on the IRS Schedule C (Form 1040) for Other Expenses. It can be confusing and hard to find information on what business deductions can be listed in this general category. This is a great reason to consult a CPA to confirm what is considered an ordinary and necessary expense in your field of business. Examples of other expenses that your bookkeeper or accounting software may track include: internet, cell phone, bank service charges, dues & subscriptions, annual renewable computer software, shipping & delivery, and continuing education.

If you decide to do your own taxes, be sure to have at least one meeting with a CPA to confirm what is considered ordinary and necessary business expenses for your business.

Chapter 5.3: Home Office: Can You Really Write It Off?

Do you primarily work from home? If so, do you claim the home office deduction or are you scared that it will raise a red flag with the IRS? I’ve talked to many small business owners who are so afraid of an IRS audit that they choose not to claim home office expenses, but they could be giving the IRS more money than they owe! Don’t cheat your business out of money that you can legally keep and invest back into the business (or pay yourself). Consult with a tax professional to discuss your specific situation to understand if you meet the qualifications for claiming home office expenses.

According to the IRS.gov website, several criteria must be met to qualify for deducting expenses for business use of your home, including 1) exclusively and regularly using it as your principal place of business, and 2) exclusively and regularly as a place where you meet or deal with patients, clients, or customers in the normal course of your trade or business. The key word here is “exclusive.”

If you do qualify for a home office deduction, there are two methods you can use: the simplified option or the itemized deductions.

- Simplified: Deduct $5 per square foot of the home office (up to 300 square feet)

- Itemized: Per the IRS, claim actual home-related expenses such as mortgage interest, real estate taxes, and utilities.

Itemized expenses that can be included in your home office deductions include direct expenses for the business part of your home and indirect expenses for maintaining and running your entire home. Check out Publication 587, Business Use of Your Home for the most recent revisions. Examples include:

- Direct: Painting or repairs in your home office.

- Indirect: Home insurance, utilities, and general repairs.

The IRS provides general guidelines, so I recommend confirming with a CPA on what expenses you can and should include for your home office. For example, I track my monthly alarm system fees, homeowner association dues, homeowner’s insurance and umbrella policy premiums, pest control, and weed control. I have one phone line that I set up to take business calls, but was told by my CPA that I needed a second phone line to justify a business deduction for the monthly bills.

Example: Let’s look at which method is better if your home office is 150 square feet, the total square footage of your home is 2,800 square feet, and your total home office expenses totaled $18,000:

- Simplified: $5.00 x 150 square feet = $750

- Itemized: (150 square feet / 2,800 square feet) * $18,000 = $964

- Answer: Itemizing is the greater deduction by $214.

- Alternative: If you don’t want or have the time to gather, calculate, and keep records of all the home office related expenses, then doing the simplified method works great too during crunch mode.

Regardless if you use simplified or itemized, just be sure that you follow the IRS definition of exclusively and regularly use the space for your business. In other words, don’t have a pull-out couch in your office and allow out-of-town guests to sleep in there! I’ve heard and read stories about business owners who claimed a home office, but were audited and not allowed to take the deductions because they let guests sleep in their home office a couple times a year.

Chapter 6: Best System to Keep Track of Business Expenses and Receipts

Do you hate dealing with the back office stuff and put off dealing with business expenses and receipts until tax time? Deciding upfront how to manage business receipts may not be fun, yet it’s important to set up a good system and process before things get too busy. Tossing receipts into a shoebox and thinking that you will get to it later when you have time, will lead to “the shoebox problem.” That is, a box full of jumbled receipts that never stops filling up. The IRS has up to five to seven years to audit your business. In the event of an IRS audit or if your CPA has questions on specific business expenses during your tax preparation, you will need a system to easily track and find receipts. Otherwise, if you have incorrect or no documentation, the IRS will calculate penalties and interest on the amount that was due at the time of the tax return.

Chapter 6.1: Top 3 Reasons Why You Need to Use the Cloud

Are you currently saving all your files directly onto your desktop? Avoid the costly mistake of storing all your critical business files — such as signed contracts and business receipts— on your desktop, without a backup. A virtual storage system through the cloud is one of the best ways to store your important business data for a relatively low cost. Top three reasons include:

- If your laptop is stolen or your computer crashes, you will lose all your important company and client data, and not have a recoverable duplicate. Imagine the wasted hours, stress, and increased costs when you are forced to re-create or track down an immeasurable number of files. This can also put your clients’ data at risk, potentially affecting your professional credibility.

- No loss due to flooding or fire – I have heard stories where a house flooding or fire destroyed all the paperwork of a business, and business owners had zero documentation for IRS audits.

- Accessibility – When using the cloud, you can access your files anywhere you go, when you are on the road for business or decide to move.

Without organized business receipts and immediate access to critical paperwork during tax preparation, filing can be stressful, costly, and time-consuming.

Several companies offer options for cloud document storage for as low as five dollars per month or charged based on use. Examples include Microsoft OneDrive for Business; Box, Inc.; Dropbox Business; and G Suite by Google. Sign up for a free trial (most companies offer this) to test out solution before you commit to a monthly or annual subscription. In my business, I use Office 365 Business Premium for less than $15 a month.

Chapter 6.2: Who to Outsource to If You Hate Dealing with the Boring, Admin Stuff

If you don’t have the time or energy to get yourself ‘out of the weeds’ and have would rather outsource these administrative tasks, here are three options to save you time and minimize stress once you’ve decided on a cloud system.

- Personal Assistants – Research three personal assistants who can come to your office to help with gathering, organizing, scanning, uploading the receipts and paperwork to your cloud system, and shredding originals.

- Places to do research and post job postings for a personal assistant include Craiglist.org, Care.com, and Upwork.

- Records Management Companies – Consider local scanning/storage companies, especially if your industry requires you to keep all original physical records and you find that space is an issue.

- Companies like Iron Mountain or The File Depot will deliver storage cartons to your location for your records. When you are ready, they will pick up the cartons, scan, and store your files in a secure facility with alarm systems, fire detection, and security monitoring.

- Online Organization Companies – Check out companies that allow you sign up for a monthly subscription and mail in your receipts, business cards, and business paperwork to be scanned and archived in a secure location.

- Shoeboxed is a company based in Durham, NC that serves over 100 countries and scans your receipts and turns the scanned images into data that can be categorized, organized, and fully searchable.

Once your receipts and files are scanned to a secure cloud system, shred the originals. The IRS does accept digital images, provided they’re legible and haven’t been tampered with.

Chapter 6.3: How to Not Tear Your Hair Out When Providing Proof for IRS Audit

Once you have a cloud subscription, make sure to organize and save your files in a way that you can easily find what you need and when you need it. Otherwise, you could end up wanting to tear your hair out when having to search through hundreds of files to search for specific receipts during an IRS audit.

Recommendations:

1. Create a Finances folder in your cloud storage system.

2. Within the Finances folder, create a folder for each tax year (i.e. 2018, 2019, 2020, etc.).

3. Within each tax year folder, create a folder for each business expense type. (*Refer to the Schedule C (Form 1040) Part II for examples).

- By creating a folder for each business deduction type, you easily navigate to the appropriate folder to find a specific receipt if your CPA has a question about it.

- Tip: Differentiate between meals while in-town versus traveling. (*Note – most meals in-town are only 50% deductible, but most meals while traveling for a business conference is 100%. Confirm with a CPA for your specific business and situation.)

4. When saving receipts, use a file naming convention that will make it easy to find and provide receipts to CPA or IRS as needed. For example:

- Good: “Meals and Entertainment – Caribou Coffee – 2018.03.01 – $4.75.jpg”

- Not as Good – “Img_1777.jpg”

Chapter 6.4: How to Fool-Proof Your Receipts

One category of business expenses that is highly scrutinized by the IRS is meals and entertainment. If they find any issues with your recordkeeping in that category, another area of high scrutiny is mileage. Use the journalist’s approach when thinking about what information you need to record with these business expenses, often referred to as the “5 Ws”. For example:

Journalist Approach to Receipts (5 Ws):

- Who – name of the person(s) you met

- What – what was discussed during the meeting or meal

- When – date of meeting (*Note – usually on receipts for meals and entertainment)

- Where – name and/or address of meeting or meal

- Why – the business purpose of the meeting or meal

- Meals & Entertainment: If you buy coffee during a meeting with a client, write at the bottom of the receipt the name of the person and business purpose. For example, “Consultation Meeting with Susie Smith.” If it was a networking meeting, then you may want to write, “Networking Meeting with Tim Jones re: referral partnership.”

- Mileage: You can use a mileage book from an office supply store, spreadsheet, or miles app to track the number of business miles per trip. In addition to tracking the 5 Ws, make sure to record the total number of miles driven on the car(s) too. (*Refer to Chapter 10: Make Your Drive Worth It in Small Business Finance for the Busy Entrepreneur – Blueprint for Building a Solid, Profitable Business for more detailed information on tracking business mileage or reporting actual expenses for car use.)

The more information and details that you have documented upfront, the more likely that your receipts and records will hold up in an audit. If you haven’t done a good job of keeping records, you can start now.

Chapter 7: How to Pay Your Taxes, and Not a Penny More

Understanding what constitutes a deductible business expense can be extremely confusing. You may not realize that something can be claimed as a business expense, and toss away those receipts. By the time you find out, either by engaging with a CPA or through a financially-savvy colleague, it is too late to claim those tax deductions. If you decide to do your own taxes to save the $500 or more in CPA fees, you most likely err on the side of caution, and won’t deduct expenses that may raise a red flag. Also, given tax laws can change, deductions that you can take one year, may not be allowed the next. Estimating taxes and quarterly payments are another area that can be confusing, which can lead to not paying or saving enough. If you aren’t paying enough estimated taxes, that can also lead to penalties. Make sure you hire the right professionals to ensure you’ve paid your fair share of taxes, but not a penny more than you need.

Chapter 7.1: Don’t Overpay Your CPA

When working with a CPA to prepare your taxes, there are four things to keep in mind:

- Hire a CPA who is focused on tax services for individuals and businesses. Some CPAs don’t focus on tax preparation and are only specialized in audits or financial services. You want a CPA who has experience preparing tax returns and can represent you in the event of an IRS audit.

- Do not physically hand over a box of receipts to a CPA. Depending on your CPA’s policy and interpretation of the tax standards (Statement on Standards for Tax Services No. 3 – AICPA), he or she may decide to manually count all the receipts and not take your word for any totals given! Remember that CPAs charge for their time, and this is an expensive administrative task for them to do, especially if they charge $175 – $200 per hour! (*Note – if you have a shoebox of receipts, be sure to read Chapter 6: Best Systems to Keep Track of Business Expenses & Receipts for solutions.)

- Make sure all your business expenses are separated from personal. Don’t give the CPA a data dump of an entire year’s worth of bank transactions and expect him/her to sort through and know which ones were personal versus business. Only you would have knowledge of what you did or purchased, so they would only be guessing and flagging any line items to have you answer or research. (*Note – If your finances are commingled, make sure to read Chapter 2: Separate Your Business and Personal Finances (Or Pay the Price) to find out solutions.)

- CPAs are not mind-readers. While most offices have organizers that they will send you to assist in gathering information necessary to prepare your tax returns, only you know of major events that happened in your personal life and business, such as home renovations that qualify for an energy tax credit. Or, you gave away 50 copies of your books for marketing purposes, and the cost of books should be deducted. Be sure to point out major events to confirm if any affect your tax liability.

Chapter 7.2: Who You Should Hire and Have in Your Corner

There are lot of people who can help with finances and taxes, but there are distinct job descriptions and qualifications to understand. Here are people to consider hiring and having in your corner as you build and operate your business:

- Certified public accountant (CPA): an accounting professional who has passed the Uniform CPA examination given by the American Institute of Certified Public Accountants, fulfilled the work experience requirements, and has met state certifications and requirements.

- Accountant: trained in bookkeeping, auditing, preparing of financial reports and statements, and can advise on tax laws and investment opportunities.

- Bookkeeper: a person who can record financial transactions of a business, such as sales, purchases, payroll, collection of accounts receivables, and payment of bills.

- Financial Advisor: a professional who provides financial services, products, and advice related to investing, retirement, insurance, mortgage, college savings, estate planning, and taxes.

- Financial Coach: focused on educating, sharing best practices around financial management, and providing accountability to achieve goals. Can help a client identify areas to reduce spending to create more savings and get out of debt.

Chapter 7.3: Frequently Asked Questions

- I don’t think it’s worth it to hire a CPA. Can I just use Turbo tax?

- Tax software like TurboTax can be fine when you have a simple tax return or don’t need to itemize your deductions. However, I recommend that business owners hire a CPA to ensure they are taking the maximum deductions allowed, especially when there are significant changes in their personal lives or business.

- Real-life example: In the past, I’ve compared what my CPA calculated for my tax return versus using TurboTax, and often I missed one or two items that I didn’t realize were eligible deductions. One year, I didn’t know that a new investment vehicle set-up by my financial advisor required me to complete a Schedule K-1 form and file a New York state tax return, in addition to my home state. Had I not hired my CPA, I would have been fined for not filing a tax return for income earned in New York. This is a great example where financial advisors may not always know the tax implications for investments that they recommend, so it’s always a good idea to check with your CPA before investing in out-of-state investments.

- Should I hire a CPA or a bookkeeper?

- A bookkeeper does not need any certifications and can be fulfilled by anyone who is good at keeping detailed financial records and transactions. This person cannot represent you in the event of an IRS audit. On the other hand, a CPA can prepare tax returns and must meet initial qualifications and complete state specific number of hours of continuing professional education to maintain certification. CPAs can represent their clients before the IRS, and advise clients during audits.

- Why are my CPA fees so high to file a tax return?

- If you aren’t organized and your CPA has to keep asking you for missing documentation, he has to stop preparing your tax returns until you send them in. In the meantime, he’s moved on to other tax returns. When you finally send in your missing documents, he needs to go back to your tax return and remember where he left off. This stop and re-start can take additional time versus if your CPA processed your taxes in one sitting. Therefore, you end up compensating your CPA for the extra time.

Regardless if you (or a family member) want to do your own taxes and use a tax software, it’s worth the investment to hire a CPA for at least for a one hour consultation to answer any questions and validate assumptions that you have regarding business deductions and tax rates. Be sure to prepare for that meeting by creating a list of questions and send it ahead of the meeting so the CPA can be prepared. Given that you will likely being charged by the hour (average $200 per hour), planning upfront can save you time and money.

Chapter 8: How to Make Tax Day a Piece of Cake (and Eliminate Need for Tax Extensions)

If you work for a company, your employer paid your federal and state taxes. When you receive your paycheck, those taxes were already taken out on your behalf, so no action was needed on your part. Now, when you have your own business and make a sale, the client pays you and you receive the full amount at the time of the sale. No one has taken taxes out yet. This is where many small business owners make their mistake. Since there is not a standard guideline or requirement for how this money gets set-aside (because the government only looks at receiving its money), many small business owners spend all of that money (before taxes), not realizing the cost of not saving for taxes … until, that is, they get their first big tax bill! By having a separate checking account for taxes and regularly transferring money from your primary checking account based on your tax rate, you will never have to worry about running out of money to make your tax payments.

Refer to Chapter 3: The 3 Types of Bank Accounts You Should Absolutely Have if you don’t have an account dedicated for taxes.)

Chapter 8.1: Top 10 List When Meeting Your CPA

When meeting with your CPA to prepare your taxes, here are a list of top ten items that you should bring:

- Income – proof of all income earned, including W-2 and 1099-MISC

- Interest – proof of interest earned from bank accounts and investments, including 1099-INT forms

- Dividends – proof of any dividends received from investments, including 1099-DIV forms

- Expenses – proof of business expenses that were ordinary and necessary to operate the business. Provide the totals based on categories as listed on Schedule C (Form 1040)

- Healthcare – proof of health insurance coverage throughout the calendar year

- Mileage or Vehicle Actuals – proof of number of miles driven for business on personal vehicles, or actual totals spent to upkeep vehicle used for business.

- Business Use of Home – proof of direct and indirect expenses to maintain home office within personal home.

- Deductions – proof of eligible deductions, including medical and dental expenses, personal property taxes paid, real estate taxes, mortgage interest paid, charitable contributions, and miscellaneous.

- Summary – include summary data about your personal and business, including your legal entity of business, square footage of home office versus total house, % of internet use for personal versus business, and % of cell phone use for personal versus business.

- Questions – include any questions that you have, especially if there are any significant changes or new developments in your personal or business. It’s always better to provide more information and ask questions on tax impacts, than make assumptions. Include space to document answers from your CPA.

Chapter 8.2: How to Get the VIP Treatment from Your CPA

The best way to get VIP treatment from your CPA is to be organized! Have all your financial information organized as recommended in Chapter 8.1: Top 10 List When Meeting Your CPA. To take it a step further, if you are handing over paper copies and documentation, use a binder clip to keep all the same types of information together. When I meet with my CPA, he is always thankful that everything is so easy to find and that all the information has been provided in one meeting.

On the other hand, I know CPAs who will fire their clients if they are consistently missing documents and dragging their feet until the last minute to provide necessary files. It can be stressful for CPAs and their staff if they’ve promised to get your tax returns filed on-time, but they don’t know when you’re going to submit the data needed for them to complete the work.

Eric Nisall, an accountant for bloggers and freelancers, shared with me that his worst client would be someone who calls every day, talks 90% about non-business stuff, has a lot of drama, and who he needs to chase down because he can’t rely on them to deliver what he needs.

Another tip is to schedule your meeting in January or February, and get on your CPA’s calendar before early-March. This is before tax season gets hectic with last minute requests and delays, which cause your CPA and staff to work weekends and nights to get everyone’s taxes done on-time. I’ve found my CPA to have plenty of time for questions in February, but once mid-March rolls around, it’s hard to get a hold of him.

Chapter 8.3: Create a Financial Admin Day (FAD)

Does all of this information sound great, but you don’t know where to find the time to get organized? Schedule at least one day a month for a Financial Admin Day (FAD) for one to two hours to manage the financial side of the business. This time can include paying bills, following up on outstanding invoices, and scanning/saving business receipts for tax records. Schedule this as a recurring meeting in your calendar, and hold to this commitment like you would a meeting with a client.

Chapter 8.4: How to Never Miss an Important Deadline

Mark your calendar for important deadlines relating to taxes, and then block time with a meeting invite for yourself to work on your business finances BEFORE the due dates. Key dates that you want to add to your calendar include:

- Deadline to mail W-2 Forms and 1099 Forms – January 31st

- Estimated Quarterly Tax Payments – Based on IRS.gov website, if the due date for making an estimated tax payment falls on a Saturday, Sunday, or legal holiday, the payment will be on time if you make it on the next day that is not a Saturday, Sunday, or legal holiday.

- Business Tax Return Due Dates

- Sales Tax Due Dates – these vary by state and if you are required to file monthly versus quarterly. Go to your state’s department of revenue website to find due dates based on your business requirements.

- Annual Report Due Dates – based on your legal entity and state requirements, there are due dates to file the annual report and fees to maintain your business entity. Go to your state’s secretary of state website to find due dates. Often, you can process the annual report and pay the fees online.

Chapter 9: Overcome the Fear of Being Audited (and Learn What the IRS Really Cares About)

To overcome the fear of being audited, let’s look at the IRS mission and what they really care about when it comes to the American taxpayers. The IRS is a federal bureau within the Department of the Treasury of the United States. As Congress passes tax laws, the IRS must ensure all taxpayers comply and pay their fair share. The government uses the collected revenue to fund public services like schools and roads. Therefore, the government charges you (and all other taxpayers) an income tax based on all your income earned and received.

(*Note – Sales tax is completely different from income tax. In the United States, this is a direct tax that many states and local governments impose when you purchase goods and services. Most states (except for Alaska, Delaware, Montana, New Hampshire, and Oregon at the time of this writing) use the income received from sales taxes help fund state initiatives. Therefore, if you perform business in states that impose a sales tax, as a seller, you are required to collect the sales tax from a customer at the time of purchase, and then report and send in the sales taxes collected to those states.)

Chapter 9.1: Income You Made

Since the government requires you to pay your fair of income taxes on all your income, you need to make sure you don’t overlook any income that you earned or received each tax year. Therefore, keep good records of income received from:

- Your business

- Employer – salary, unemployment compensation

- Investments – interest, dividends

- Property – rent

- Other – Royalties, lottery earnings

As a business owner, you need to keep good records of all the sales you make throughout the year, report your earnings, and pay the IRS the taxes you owe on your taxable income.

Since your employer, banks, third party payment processors, and brokerage firms are required to report your income to the federal government, you will receive tax statements that you can use for your records to report those earnings.

Chapter 9.2: Income You Paid to Independent Contractors

When you hire independent contractors, you are now acting as the “employer,” and it is your responsibility to report to the IRS the income you paid. By doing so, the IRS has proof of the income earned by these independent contractors from you and will compare that to the earnings reported by them on their tax filings. If the numbers don’t match or the independent contractors fail to report their earnings, the IRS will go after them.

If you fail to report the income you paid to independent contractors, you are the one who gets in trouble! Therefore, before you agree to hire any independent contractor, require them to complete a Form W-9. (*Note – this only applies if you pay an independent contractor over $600 in a calendar year by cash, check, wire transfer, electronic checks, ACH, online bill pay, or direct deposit.)

Then, it is your responsibility to mail them a completed 1099-MISC form by January 31st of the following year so they can match it with their records, or risk being fined by the IRS for $50 – $520 per missing form. (*Note: Refer to the Increase in Information Return Penalties on IRS.gov for more information on penalties.)

Chapter 9.3: Taxes Are Paid

To help ensure you don’t accidentally spend your tax money and run out of money, the government typically requires a “pay as you go” system for taxes. It doesn’t want to wait until the end of the year when you file a tax return, so the government requires you to pay estimated taxes quarterly (typically in four equal installments) on income from self-employment, business earnings, interest, rent, dividends, and other sources. A CPA can help you determine your estimated payments, typically based on your income from the previous year.

If you underpay your estimated taxes, then you will have to write a check to the IRS when you file your tax return. Depending on the amount of difference, you may get penalized for underpaying throughout the year, because the IRS wants to motivate you to get the quarterly payments as accurate as possible. In the eyes of the IRS, you held onto their money that you should have paid sooner!

If you overpay your estimated taxes, then you will receive a tax refund. While it can seem great to get a refund, you don’t want this amount to be drastically high since this basically means you gave the government an interest-free loan!

(*Note – Remember to open a business checking account dedicated for your taxes as recommended in Chapter 3: The 3 Types of Bank Accounts You Should Absolutely Have.)

Chapter 9.4: How to Prove You Didn’t Cheat, Lie, and Steal

Filing a tax return is your way to report income, calculate your tax liability, and make payment or request refunds. The IRS doesn’t always have all or accurate income information, so be sure to hold onto all records that will prove the income you earned and the taxes you paid. The IRS just wants to make sure you didn’t cheat, lie, or steal any money that is owed to them.

One example for how your income may not match what the IRS has on file is when someone incorrectly sends you a 1099-Misc for income that is already being reported by your payment processor, such as PayPal. In this case, your income is double reported, but the IRS will want to fine you for not paying enough taxes. You will want to have records to prove the correct income earned.

In other words, you need to prove this:

Your $ Tax Liability = $ Taxes Paid to Government

Chapter 10: How to Survive Being Audited by the IRS

Many taxpayers fear and dread getting audited by the IRS. Being selected for an audit can sometimes happen randomly through computer screening based on a formula that compares your return against “norms” for similar returns. Then, other times it may get selected due to issues with related returns, such as business partners or investors. When you are selected, know that the IRS will initially notify you by mail, so don’t get fall for scams from someone calling you and demanding a payment to the IRS!

Chapter 10.1: 3 Types of Audits

There are three different types of audits that can happen, and learning the difference will help you know how to deal with them:

- Correspondence – this is the simplest type of audit, requesting more information about a specific section of a tax return or requesting answers to specific questions.

- Office – this is when the IRS have more questions about your return and will request that you come into an IRS office for an audit. This is typically more detailed, but the audit could be done in one day.

- Field – this is the most comprehensive audit and the IRS will visit your home or business. When the IRS visit, the agent may ask for additional items.

Chapter 10.2: Bring It On – What You’ll Need in an Audit

The IRS typically will audit up to the last three years, so make sure you keep the last three years of tax returns and records. If you didn’t keep receipts from the past, download your bank and credit cards statements. While these don’t always hold up in an audit, this at least gives you some documentation that you can provide and do further research as needed. (*Note – banks typically only keep the most recent 12 – 18 months online, so be sure to download your statements or request them to be mailed, which can take several weeks to arrive.)

- Correspondence – for this type of audit, if you have the receipts and documentation to support the questions, you will send those in and will get a letter back on the decision. You can generally handle this on your own if you have the documentation. However, if you are missing receipts and documentation, you may want to hire a CPA or tax attorney helping you deal with the IRS to negotiate and resolve it.

- Office – this will require more time and you will need to provide documentation as requested. Hiring your CPA to help with this audit can be useful to coach you and give tips on what to say and what not to do during the audit.

- Real-life story: Find out what happened when J.D. Roth, founder of Get Rich Slowly, got audited by the IRS, how much he paid his CPA to coach him through the process, and his lessons learned from having a shoebox of receipts and accidentally paying a few business expenses from his personal bank account: https://www.getrichslowly.org/i-was-audited-by-the-irs/

J.D. and I catching up after the Forefront conference

- Field – this is a bit more serious because the IRS is visiting your home or business to look around and confirm legitimacy of your business. Hire a CPA or tax professional to coach and be an advocate for you and your business.

Chapter 10.3: Possible Outcomes from an Audit

There are three possible outcomes to an IRS audit:

- No Change – everything that you submitted has been reviewed and determined that there are no changes. The audit is closed.

- Agreed – the IRS proposed changes that you understand and accepted. If you owe money, you can make payment or select a payment plan option.

- Disagreed – the IRS proposed changed and you understand but disagreed. You can request a meeting with the IRS manager, go into mediation, or file an appeal.

Chapter 10.4: Why Hiring a CPA to do Your Taxes is the Best Choice

Given the different types of audits, hiring a CPA to do your taxes versus doing it yourself with a tax software can be extremely beneficial in the event of an IRS audit. Your CPA would already be familiar with you and your business from preparing your tax returns, and can provide guidance in preparing for and during the audit. While there is a tax representation option that you can select with software such as TurboTax, you don’t have a relationship with any specific person versus with a CPA, who you can build a relationship with over the course of the business life.

CONGRATULATIONS!!

You made it to the end of this 12,000+ word guide. We’ve covered A LOT of information, but if there’s something that’s unclear, please leave a comment below and I’d be happy to answer them!

Thanks for reading the Ultimate Guide to Organizing Your Business Finances! Just one more thing…

I’ve spent weeks and hundreds of hours researching and putting this guide together, hoping that it would answer all your questions regarding how to best set up your business finances to stay organized, keep more money in your pocket, avoid nasty IRS letters and fines, and stay sane while running your business.

I know this guide can help thousands of people, and if you enjoyed it and found it helpful, I would really appreciate your help to spread the word so more business owners like yourself can hear about this guide and learn from it.

If you know anyone who…

- Is starting a business and wants to avoid common mistakes

- Is running a business but is working more hours in the business than on the business

- Is stressed about taxes, tax preparation, and needs to gain control over the finances

Then I’d love for you to send them a link to this guide on my blog. Here’s the link so you can just copy and paste it to them via email, LinkedIn, or Facebook: https://smifinancialcoaching.com/ultimate-guide-to-organizing-your-business-finances

It would also mean a lot to me if you:

- Shared a link to this guide on your LinkedIn wall and wrote one or two things that you learned.

- Shared a link to this guide on your Facebook wall and wrote one or two things that you liked.

- Shared it in any online business communities you’re a part of whose members would benefit from reading it.

Here’s the link for sharing this guide again: https://smifinancialcoaching.com/ultimate-guide-to-organizing-your-business-finances

Last but not least, I’d love if you left a comment below this blog post with your #1 takeaway (or surprise). If you have any questions for me, you can also leave them in the blog comments and I’ll respond.

Thank you for reading this guide and I’m excited to hear how this guide will change your business and finances!

16 Comments. Leave new

Wow, great guide Sylvia and I so needed some of these questions answered. Bookmarking this page to come back to it.

Thanks, Joseph! What was your #1 takeaway or surprise?

Nice article! I will work on my credit card right now. I will try to do your tips.

I totally agree with separating the personal and business finances. I think that by doing this you’ll not create a stress by figuring out if your business has a healthy cash flow. Thanks for sharing this very informative article. I learn a lot from this article. I guess a lot of other readers too.

I totally agree with what you said. I also figured out that it is really better to separate personal from business account. When I was just starting up my business I sometimes mixed it up. It really is a headache when it comes to accounting .

Thanks for sharing these. I also think that best way to organized a business it to separate pleasure from business. Even though it’s redundant to say and we heard it all the time. I think that it is really the best thing to do for easier accounting.

Thanks for sharing this article. I think that it is better too, to hire a CPA to do your accounting rather than do it yourself especially if you are not that good in accounting. CPA are good in numbers and can help you with decision making for the business to grow and succeed. This article is very helpful and informative.

I think you are right. When the finances are mixed. Business owners will definitely going to have a hard time in doing the accounting. It will definitely going to be so stressful. Thank you for sharing this article.

I believe that business needs to be organized so that it will be easier to be managed and grow. This article is definitely a big help for business owners especially for those who are jsut starting up. Thanks for sharing this very helpful and useful article.

Thanks for reading and I’m glad that you found this helpful to get organized!

Finances are very important for the business. I think that it will not grow or succeed when it has an unorganized finances. I think that we should really have to separate our finances to be able to manage it well. This is really a great article.

To me, the most valuable thing was the admonition to use cloud-based storage for records, receipts, etc. Personally, I think you should update your guide to talk about Cybersecurity – e.g. ransomware, phishing, password hygiene, etc. I know of at least (3) fellow entrepreneurs that almost had their businesses fail due to ransomware, phishing attacks, or a data breach that led to customers personally-identifying information being compromised and not realizing they needed professional help versus searching the internet for FREE solutions.

Thanks for reading, Matthew! Great point about cybersecurity! I’ve heard similar stories. Will look to include that in an updated version!

Sylvia, have you ever thought of working with veteran entrepreneurs or do you have experience in this area and helping with the special benefits – contract set-asides, preferential bidding, veteran or disabled veteran-owned businesses?

Matthew, I’m not as familiar with the special benefits offered to veterans, but I do have a colleague who focuses on personal financial coaching for veterans and their families. Otherwise, I can help with the understanding the financials, pricing, etc. of the small businesses.

I also think that it’s best to hire a CPA because I think that when it comes to finance or accounting, they know better. They are a good help for decision making. Thanks for sharing this article.